Ready to start investing in 2025? Questrade makes it easier — and cheaper — than ever. Questrade offers zero trading fees on many accounts, along

Read More

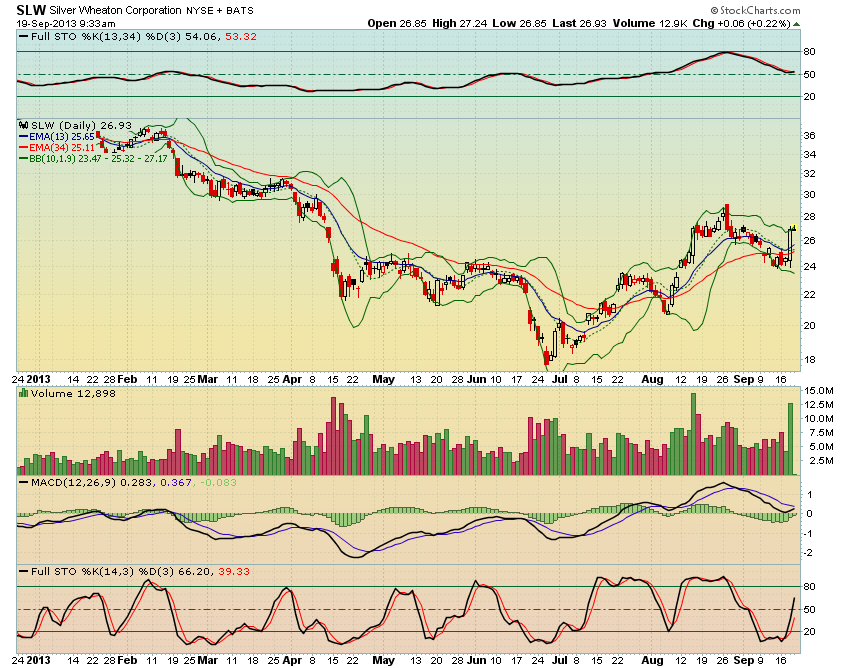

[[SLW]] Up on strong volume, second time in a month – possibly not a fluke

readI hadn’t even noticed as the US dollar crept up to $1.055 which is the current official exchange rate. Of course, actual – say, charged

readALERTS TO THREATS IN 2013 EUROPE From JOHN CLEESE The English are feeling the pinch in relation to recent events in Syria and have therefore

readOver the past few sessions, volume pattern has turned very bearish. There are now 2 gaps on SPY – one gap down which will probably

readI don’t remember if I already blogged about this, but anyway – recently I was looking into peer-to-peer lending. My friend moved to the States

readI couldn’t wrap my head around binary options for some time, but now I get it… I think. Here’s a plain English explanation if you’re

readI own a couple of bars minted by Valcambi (via Scotiabank). I used to think that all gold bars were minted by Credit Suisse 🙂

readWhen I hear the phrase “real estate community”, I think of “The Glades” episode about a nudist colony. Also, my friend in Florida comes to

readGuess who is making more money on mobile ads: Facebook [[FB]] Google [[GOOG]], or Linkedin [[LNKD]]?

readView More